|

|

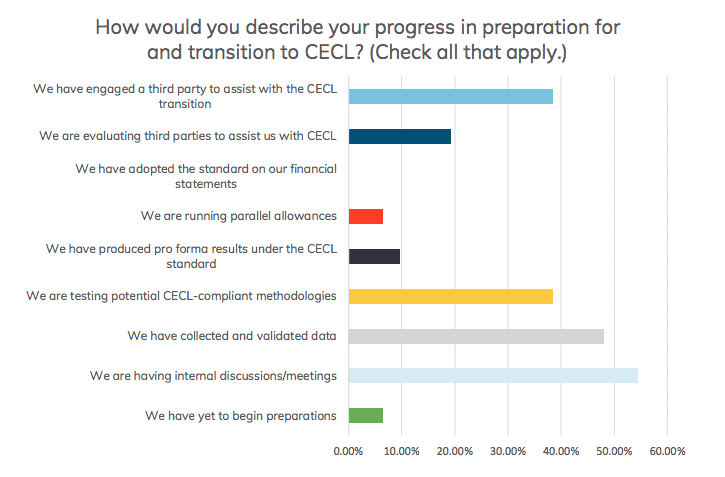

With nine months left to implementation, only 14 percent of SEC registrants are currently running parallel loan loss allowance models under the new current expected credit loss accounting method, while 3 percent of SEC registrants acknowledge they have not yet begun CECL preparations at all.

That’s according to the third annual CECL survey from Abrigo, a technology provider of compliance, credit risk and lending solutions for community financial institutions gauging financial institutions’ preparedness for the upcoming transition to CECL

The survey included responses from institutions located or doing business in every state in the U.S. and from institutions representing a variety of asset sizes. Survey participants include presidents, CEOs, CFOs, chief risk officers and chief credit officers, senior vice presidents, controllers, various vice presidents and credit or loan executives, as well as numerous risk and financial analysts.

The 2019 CECL Survey shows that as the the first quarter of 2020 compliance date nears for SEC-filing institutions, progress is being made across the board – but not fast enough, according to CECL experts.

“The clock is ticking,” Regan Camp, senior director of advisory services at Abrigo said in a statement. “While many financial institutions are taking the necessary steps to make sure they are prepared for this important change in accounting for credit losses, it’s clear that others are falling behind their peers.”

In addition to gauging financial institutions’ preparedness for the transition, Abrigo also assessed the personnel involved in CECL preparations, the depth and breadth of data collected, and the methodologies financial institutions are considering using under CECL during the survey.

The survey showed differing results between SEC filers, community and mid-market banks, and credit unions. The array of methodologies selected by financial institutions suggests that there really is no “one-size-fits-all” approach to achieve CECL compliance.

Forty-three percent of survey respondents said their accounting departments were the main drivers behind CECL preparations, while 25 percent said their credit departments were the main driver.

More than 40 percent of respondents said they were using a cumulative loss rate analysis to calculate reserves based on CECL, but about 37 percent of respondents said they haven’t identified potential methodologies yet.