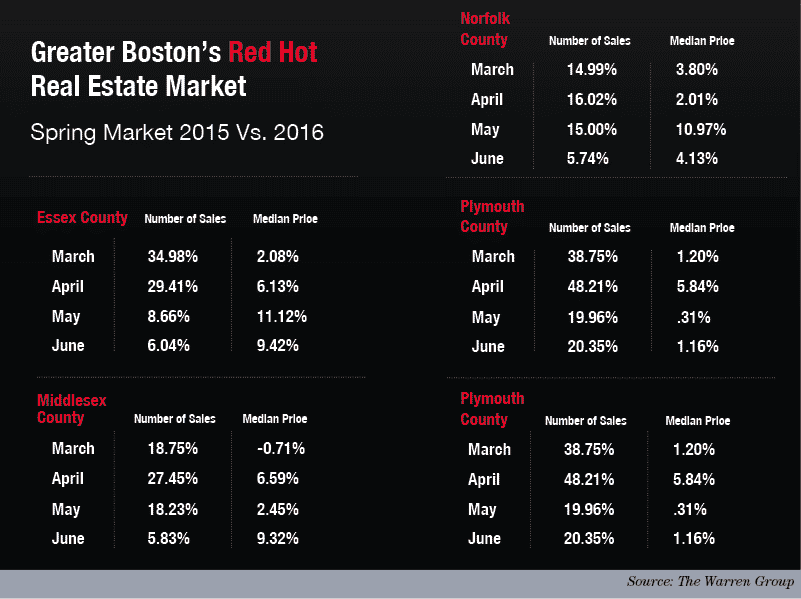

The white-hot Greater Boston real estate market is generating a lot of heat, and a lot of money, but it’s not making everyone feel all warm and fuzzy.

If 2015 was a strong year, 2016 was a very strong year for Massachusetts real estate – and 2017 looks even better. Realtor.com chief economist Jonathan Smoke predicts prices and the number of sales will both increase just over 6 percent in 2017.

That growth is expected to depend on rising, but still historically low, mortgage interest rates. Mike Fratantoni, chief economist and vice president of research for the Mortgage Bankers Association, expects mortgage interest rates to remain relatively low throughout 2017.

Homebuyers Hit Hardest

Gary Dwyer, broker/owner of Buyers Agents of Boston, said it’s harder to get an accepted offer for his clients now than it has been at any time since he started his company in 2005.

“For the past five years it’s been a challenge, especially for first time buyers, to get them to the closing table,” Dwyer said. “They come programmed to buy a house like their parents did, except now it often takes three or four offers to get one accepted. Buyers get frustrated and feel like they’re being taken advantage of by sellers and agents. They’re often unwilling to take an agent’s advice on a bid; they listen to friends and family.”

He tries to explain all that up front so when his clients see a home they want, they’re prepared to go through the process. Despite his advice, some buyers let the frustration of losing out on bids wears them down and they make risky decisions.

“It’s not uncommon for frustrated buyers to waive inspection, mortgage and condo document review contingencies,” he said. “That’s very risky and dangerous. It puts their deposit at risk. That’s a big chunk of change. I’ve had buyers make those sacrifices, but I tell them to speak with their attorney and loan originator so they understand exactly what the ramifications might be.”

Mortgage and home inspection contingencies are designed to protect buyers and in a balanced market they’re considered just another part of the offer – but in the currently frenzied sellers’ market, they’re considered weaknesses in a prospective offer.

Dwyer encourages his buyers to offer more than the asking price to increase their chances of being successful, but he knows if his clients get the house and have to sell soon – or if the market turns – they risk losing a considerable amount of money.

“When I’m talking to clients I ask them what their time horizon looks like,” Dwyer said. “If they’re planning to move in three years, it might not be a good time to buy. You want to have at least a four to five year horizon to ensure you at least break even.”

Rising home prices and competition is pushing buyers out further from the city than they’d like to be, increasing commuting time and costs as well.

“You might have someone who starts in Jamaica Plain and after seeing what their money can buy there, they might move their search out to West Roxbury or Dedham,” Dwyer said. “Or Cambridge buyers go to Somerville or Arlington or beyond. It can be less busy out there, depending on the price and condition.”

With the rise in mortgage interest rates comes a near-halting of the years-long refinancing boom. Those loan originators who have subsisted on the refi business and not developed the purchase side of their business are going to find themselves out in the cold, said Amy Tierce, regional vice president of Wintrust Mortgage.

“It is very important for loan originators to keep their business well balanced between referrers,” Tierce said. “Realtors have more influence on transactions than ever. They remain an important part of our business. If you haven’t started to generate that business, it’s almost too late to start.”

There will always be refis in any market, but a strong purchase market is more stressful on loan originators than a mix of purchase and refinance customers. Due to the nature of the transaction, purchase clients can be more challenging.

“Managing lots of negotiations throughout the week can be a lot of stress,” Tierce said. “There are lots of anxious buyers and agents. The top-producing loan originators are having these conversations up front. What happens if I increase my offer another $10,000 or $100,000? Don’t throw away your rights like your mortgage, appraisal and home inspection contingencies. It’s emotional and everyone wants it to move fast. You can be working all day and all night when the market ramps up.”

Appraisers are feeling the pressure, too. A graying industry with high burdens to entry, there aren’t enough appraisers to go around in Greater Boston’s real estate market.

Residential real estate appraiser Rick Lipof, of Lipof Real Estate Services, said he was extremely busy in 2016 and at times took three or four weeks to turn an appraisal around. Lipof said the growing appraiser shortage coupled with more home sales will make appraisals even more expensive – and they’ll take longer to do.

“I tell clients I don’t have appraisers folded up in the closet that I can take out when your volume triples,” Lipof said. “You must be realistic and tell your staff it’s going to take longer. They got used to the new cadence of three to four weeks. It’s very difficult to increase your staff as volume increases.”