Today’s guest post comes from the team at Down Payment Resource, an Atlanta-based company that connects homebuyers, Realtors and lenders with resources to get buyers into homes.

Atlanta-based Down Payment Resource, the nation’s only databank for homebuyer programs, released its Third Quarter 2015 Homeownership Program Index. The volume of programs increased to more than 2,400, making it the fourth consecutive increase in programs.

The index reveals the wide range of homeownership opportunities available for homebuyers across the country. Recent surveys, including the America at Home survey by NeighborWorks America, show that consumers have the desire to buy, yet many are unaware of all their home financing options, the home buying process and may overestimate the down payment and home maintenance costs.

“Today’s consumers are motivated to buy, but the down payment continues to be a primary obstacle. Most homebuyers don’t know to look for or ask about homeownership programs that could help them both in the short and long term. The requirements and benefits of programs vary greatly and may help buyers save on their down payment and closing costs, gain a lower interest rate or enjoy a healthy tax credit for the life of their loan,” said Rob Chrane, CEO of Down Payment Resource.

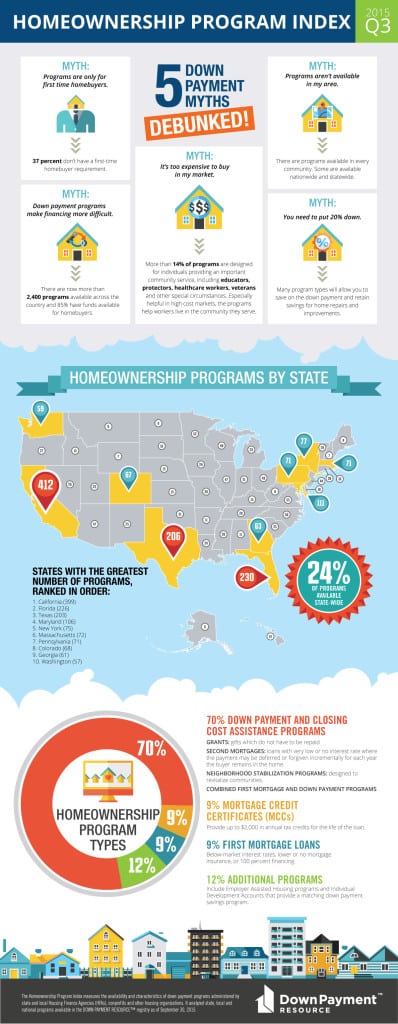

Five misconceptions about down payments may be keeping buyers on the sidelines for longer than necessary.

Myth 1: Programs are only for first-time homebuyers. While first-time homebuyer programs may be common, it’s important to note that the definition of a first-time homebuyer is someone who has not owned a home in three years. In addition, the index finds that 37 percent of programs do not have a first-time homebuyer requirement.

Myth 2: Homeownership programs make financing more difficult. There are now more than 2,400 programs available across the country and 85 percent have funds available for homebuyers. It’s important for new buyers to seek homeownership education. It’s often a requirement for down payment programs and it gives buyers confidence with the home buying process, financing options, including down payment programs, and budgeting.

Myth 3: You need to put 20 percent down. Today, a 20 percent down payment is not required and depending on the buyer’s situation, it may not be optimal. Homeownership programs allow buyers to save on the down payment and retain savings for home maintenance and improvements. Today’s programs include grants, first mortgages with below-market interest rates and annual tax credits.

Seventy percent are down payment and closing cost assistance programs. Programs include grants which do not have to be repaid, second mortgages with a very low or no interest rate where the payment may be deferred or forgiven incrementally for each year the buyer remains in the home and Neighborhood Stabilization Programs designed to revitalize communities that have suffered from foreclosures, high unemployment and other concerns slowing housing recovery. Combined first mortgage and down payment programs, typically from state housing finance agencies are also included.

Nine percent are first mortgage loans with below-market interest rates, lower or no mortgage insurance, or 100 percent financing.

Nine percent are Mortgage Credit Certificates (MCCs) that provide up to $2,000 in annual tax credits for the life of the loan.

Twelve percent are additional programs, including Employer Assisted Housing programs offered by employers in certain markets and Individual Development Accounts that provide a matching down payment savings program.

Myth 4: Programs aren’t available in my area. There are programs available in every community across the country – rural and urban. It’s important for buyers to search for programs early in their home buying journey because it may help determine the most affordable part of town or price point.

There are 19 programs available nationwide.

Twenty four percent of programs are available state-wide, offering broad opportunities not specific to a county or neighborhood. State-wide programs can often be layered with local programs.

States with the greatest number of homebuyer programs, ranked in order:

- California (412)

- Florida (230)

- Texas (206)

- Maryland (111)

- New York (77)

- Massachusetts (73)

- Pennsylvania (71)

- Colorado (67)

- Georgia (63)

- Washington (59)

- Complete list of state-by-state data.

Myth 5: It’s too expensive to buy in my market. More than 14 percent of programs are designed for individuals providing an important community service, including educators, protectors, healthcare workers, veterans and other special circumstances. Especially helpful in high cost markets, the programs help workers live in the community they serve.