Tenants’ options for new office properties in the Boston suburbs is limited. One notable exception is Hobbs Brook Management’s 507,000-square-foot development at 225 Wyman St., which is the largest contiguous block of office space on Route 128. Image courtesy of Gensler

While recent urbanization trends have undoubtedly benefited Boston’s central business district (CBD) office market, the suburbs remain dynamic as well. Looking ahead to a new decade in 2020, suburban office users will continue to gravitate towards quality modern office space as tenant experience and talent retention remain key drivers of business decisions.

It’s no secret that tenant preferences have shifted this cycle, with office users following young talent to more urban locations. Tenants like PTC, Alexion, Philips and Bose have decamped all or some of their suburban locations for new addresses in the CBD. As a result, suburban office vacancies have remained relatively flat over the last five years following steady improvements during the first half of the most recent recovery.

However, not all suburbs are created equal. The market’s innermost suburbs, including Somerville and Charlestown, have fared better than average due to their proximity to Boston’s CBD. These markets will remain relief valves for office users in search of access to talent, public transit and comparative rent value.

As the metro’s Millennial population ages and the bulk of this cohort begin to make their move into the suburbs, areas closer to the city with a more urban, walkable feel will benefit first.

Newer Product in Demand

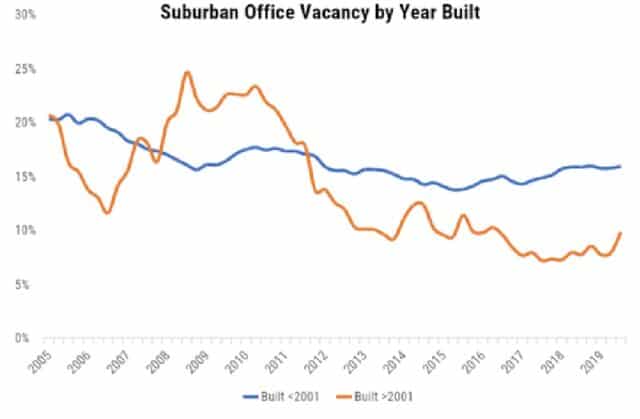

Office users also have their sights set on newer product, which there is very little of in Boston’s suburbs. In fact, office properties built prior to 2001 account for more than 85 percent of the total suburban inventory. Only 15 percent of current office inventory in the suburbs was built within the last 20 years or so. Tenant preferences for this newer space are evident when looking at recent market statistics. According to NKF data, vacancies among properties built in 2001 and sooner are roughly 6 percent lower than those among the older suburban product and have been trending downward for the better part of the last 10 years. Moreover, 3.4 million square feet of this newer product was absorbed over the last five years.

Data courtesy of Newmark Knight Frank

New development is likely a major driver of this trend, with tenants like Wolverine, TripAdvisor and Simpson Gumpertz & Heger relocating to newly built suburban offices in recent years. With that said, there is an overhang of office space built prior to 2001 as negative net absorption totaled more than 800,000 square feet during this same timeframe.

As previously discussed, proximity to Boston’s CBD is also a key factor when looking at office fundamentals. The Interstate 495 belt has higher office vacancies in general with that in space built prior to 2001 hovering above 22 percent for the last two years. Moreover, vacancies have been on an upward trajectory for much of the last decade and are now 470 basis points above their 2009 levels. While older product in the Route 128 belt has higher vacancy than newer product in the area, vacancies are in the low-to-mid–teens and well below their 2010 peak of 19.3 percent.

Walkable Inner Suburbs Well-Positioned

In order to attract and retain talent, office tenants continue to seek out well-located, highly-amenitized space. As the metro’s Millennial population ages and the bulk of this cohort begin to make their move into the suburbs, areas closer to the city with a more urban, walkable feel will benefit first. Backfilling older, more traditional office campuses will likely remain challenging as time moves forward.

Liz Berthelette

Turning to pricing, unsurprisingly, there is a significant rent premium for this newer space. This premium ended the third quarter of 2019 at nearly 21 percent, with asking rents averaging more than $31 per square foot among suburban office properties built in 2001 or later. Lease rates have been steadily rising throughout the suburbs’ older office product as well – surpassing $26 per square foot during the third quarter.

With less than 1 million square feet of product currently underway, the suburbs will continue to face a dearth of new office space. If tenant demand remains steady, vacancies in this segment of the market could tighten further in the coming quarters.

Elizabeth Berthelette is director of research at Newmark Knight Frank in Boston.