Was it something we said? The past month has seen not one, but two, multitrillion dollar banks pulling certain operations out of Massachusetts, but judging from the local banking scene, it’s unlikely they’ll be missed.

“I think the big banks are making another prototypical big bank mistake: They look at a trend in the future and never go beyond one degree of cause and effect,” said Don Musso, president of the New Jersey-based bank consulting firm FinPro.

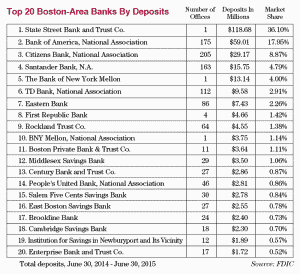

He’s referring, first, to the recent news that Citigroup will yank its retail operations out of the Boston market early next year, shuttering 17 branches in favor of greener pastures in Chicago, New York and D.C. Boston ranked 18th in deposit share, averaging a paltry $54 million, for Citigroup, while its other markets averaged around $155 million in deposits.

Though the $1.89 trillion-company stressed that it would be keeping its other lines of business in Boston – like commercial banking and private banking – a spokesman also said that Citi would only be making mortgage loans in Massachusetts via digital channels from now on.

Musso said Citigroup and other as-yet-unnamed banking behemoths may be making a fatal bet where the Millennial generation is concerned. They’re gambling that they can hang onto those consumers’ banking relationships through digital channels, and the way Musso sees it, that may not pan out as they expect.

“The big banks are making a bet that retail customers, particularly Millennials, are going to be relationship-driven through digital tech, not face-to-face, not with humans. They’re going to go after the business space and the government space and all that, but [they’re] going to go after the retail space with digital technology,” he said. “If community banks can come in and establish that real, core, person-to-person relationship, I think they can steal the retail business.”

Something In The Water?

David O’Connell, a senior analyst with the Boston-based Aite Group, sees it a bit differently. He says the market in Massachusetts – and in Boston in particular – is both attractive and difficult.

On one hand, this particular market is home to many educated, wealthy and sophisticated people. Massachusetts boasts a fairly diverse (and therefore stable) economy, too, with plenty of medical, high tech and education.

But on the flipside, the cost of doing business here is high. That, coupled with razor-thin margins that have plagued the banking industry for years, and a few more quirks of the market might mean it’s just not worth it for bigger banks to keep putting up the fight for market share.

“It is super provincial,” he said. “People tend to do business with folks from their parish or with whom they went to college. Most of the people who were born and raised here tend to stay here, and that makes it hard to break into the market.”

Not long after the news about Citigroup came the news that Bank of America was apparently dropping some of its municipal accounts with smaller Massachusetts cities and towns, including the cities of Fitchburg and Fall River.

But if BofA is dropping some of its municipal clients, community and regional banks are more than happy to talk to those spurned school districts and cities. The Bridgeport, Connecticut-headquartered People’s United Bank, for instance, is looking to beef up its government banking business and says that those jilted municipal clients exactly fit its customer profile.

Presently, the bank has around $1.3 billion in deposits in its government banking business across New England. In Massachusetts alone, it has $350 million in deposits across various cities, towns, school districts and housing authorities, said Massachusetts President Patrick Sullivan.

“When opportunity knocks, we take advantage of it,” Sullivan. “To me, it’s become another nice prospect list for us. We’re in the process of signing up two or three clients that are coming from that competitor.”

Sullivan, himself a born-and-bred New England banker, said that when cities and towns go shopping for a new bank, they often want to know more than just the banking basics. They ask how many mortgage loans the prospective bank has made in their community, how many small business loans they’ve made, what kind of philanthropic efforts, and so forth.

And that dovetails nicely into one of O’Connell’s broader points about banking in the Bay State.

“I think that individual bankers with strong local networks will benefit from these departures,” he said. The behemoth banks, he said, “have to talk someone into taking their residential mortgage away from the guy at Wellesley Bank with whom they were altar boys back in the 70s. … That’s actually a really good vignette for banking in Massachusetts.”