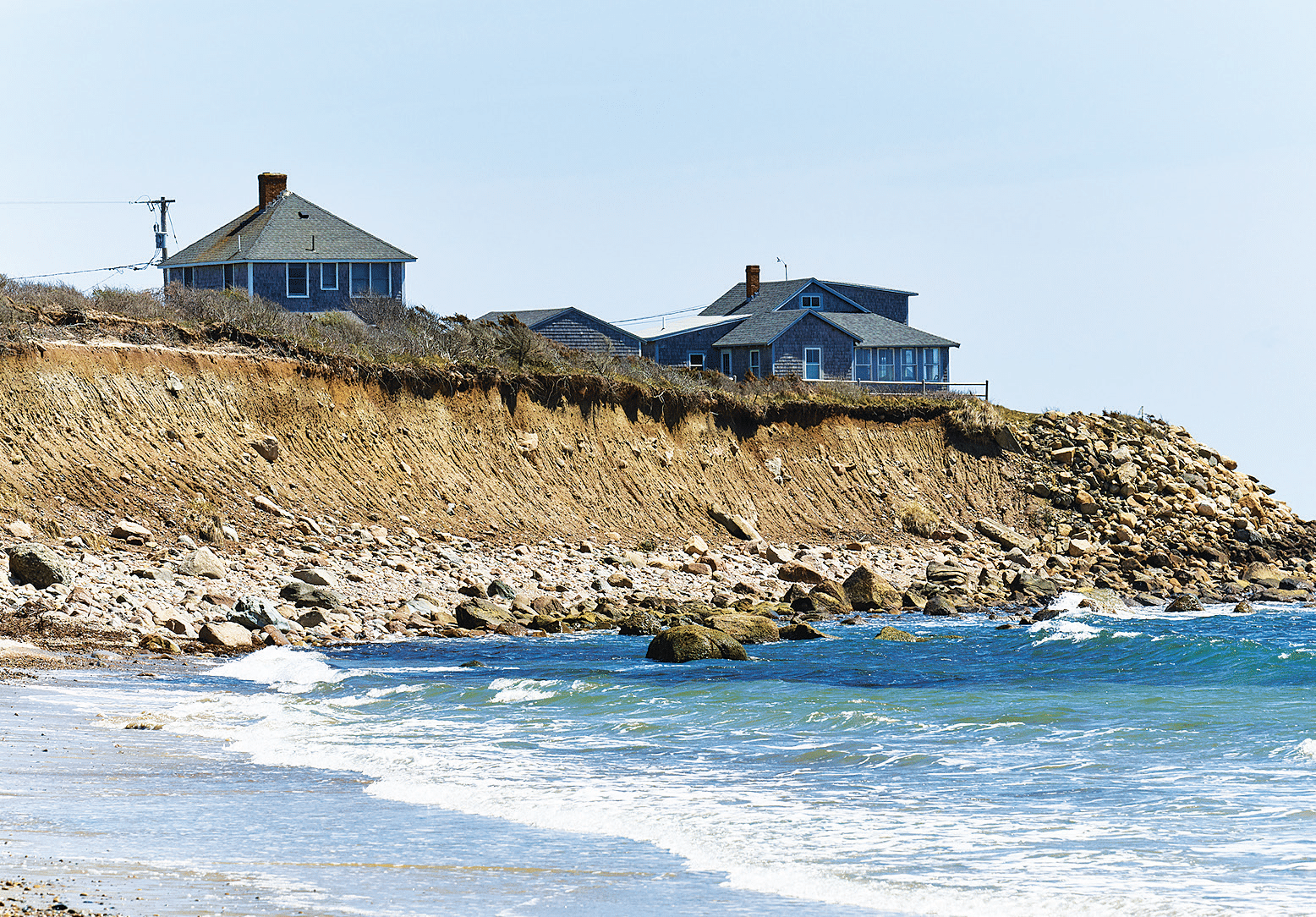

Vacation homes sit on a bluff overlooking Buzzards Bay in Westport. While coastal flooding from hurricanes has dominated much of the conversation about flood risks, inland flooding from severe weather made worse by climate change has emerged as a relatively uncharted risk. iStock photo

Worsening extreme weather, linked to climate change, is bringing catastrophic flooding to homes that have never seen it before, and it’s putting financial institutions risk of serious losses.

The biggest culprit, as identified in a recent report on banks’ exposure to climate risk, is a serious weakness in the nation’s flood insurance system.

First Street Foundation found that 57 banks in the United States with a total of $627 billion in real estate loans could face material financial risk from climate change, although it did not publicly name them. Seven of these banks are in New England.

The report also found that regional and community banks face the most pressure given the geographically concentrated nature of their lending portfolios.

Using a risk model it developed, First Street analyzed 191 banks in the country that have 20 or more branch locations. Using branch locations as a proxy for a bank’s lending area and its previous assessments of flood threats to estimate risk to mortgages held by each institution, First Street was able to identify banks that might have climate-related risks that are reasonably likely to pose a material impact on their financial condition, and hence could be subject to the Security and Exchange Commission’s proposed climate disclosure rules.

“Through climate risk financial modeling, we are able to get the first glimpse of the financial institutions which have material financial risk from their exposure to the physical impacts of climate change,” said Jeremy Porter, head of climate implications at First Street, “While this risk is material by definition, banks are finally in a position where they can proactively manage these risks to dramatically change their risk profile over time.”

Swansea-based BayCoast Bank executives say their bank is an example of a mortgage lender that is taking climate change and climate risk seriously. They have recently created a climate heat map to analyze the bank’s lending portfolio, and the bank also analyzes how various natural disasters affect its customers and tits residential lending.

The lender identified 55 loans in that area worth about $7.2 million that were impacted by Hurricane Helene.

Flood Map Problems Put Banks at Risk

If homeowners aren’t properly insured or don’t have flood insurance, they can face massive repair costs or lose their home entirely with no financial fallback.

But this isn’t just a problem for homeowners. The financial institutions that provided mortgages for these homes can find themselves with a borrower under serious financial stress or, in the worst case, a borrower unable to repay their loan.

It’s even possible a homeowner might walk away from a property in the future if homes remain improperly insured, said Gary Vierra, senior vice president and chief risk officer at BayCoast

And, unfortunately for mortgage lenders, the federal resources that should be making sure homeowners are adequately insured are not being properly maintained. A 2023 report from First Street found that around 15 million properties in the U.S. not covered by a Federal Emergency Management Agency flood map are at risk of losing insurance coverage due to flood risk.

“People that were going to buy a new home, oftentimes, relied on FEMA zones as their sort of truth for flood risk,” Porter said. “We know FEMA zones are outdated. They only cover something like 45 percent of the actual flood risk across the country, and so they’re not the best source for that.”

For example, only 12 of BayCoast Bank’s 55 loans impacted by Hurricane Helane were within FEMA-designated flood zones.

These flood maps are crucial as homes within flood zones are required to have flood insurance. But that insurance is expensive, thanks in part to the high values of the homes it has to pay for in the event of a disaster.

In recent years, FEMA has implemented a new National Flood Insurance Program pricing approach, called “Risk Rating 2.0” intended to more accurately reflect the costs of insuring homes in existing flood zones. Under these revamped guidelines, the median “risk-based” premium in Massachusetts according to FEMA was at $1,762 up from $1,106.

A possible solution to bring down those premiums, offered by Laurie Goodman of the Urban Institute, is to make flood insurance required for all homeowners, thereby increasing the pool of people paying into the National Flood Insurance Program. While people living outside of risky areas might be averse to paying more when buying a home, she noted that their costs will be lower if there are remote chances of flooding occurring in a locality.

Sam Minton

Banks Look to Avoid Concentrated Risk

For now, some local financial institutions are trying to protect themselves with an old tactic: diversifying their lending portfolios and avoiding concentration of risk.

“It’s a little bit like diversifying your investment portfolio. You can’t put too many eggs in one basket,” said Robert Talerman, president of Cape Cod 5. “It’s all about managing exposure. You might get to a point where you can’t do more of this [lending] in this area, because you’re at your exposure cap. So, we obviously look very carefully at the exposure in special flood hazard zones and those coastal high-hazard zones.”

First Street’s Porter said that small and regional banks shouldn’t reduce lending to their communities but should look to spread out the risk in their lending strategies.

“It’s not that you’re going to stop lending to your community, especially if you’re a community bank,” Porter said. “Just having that information [about climate risk] gives banks the ability to make relatively simple decisions around investment and how to start diversifying that risk on the climate side on top of all the other risk metrics that they’re already taking into account on the bank side.”

Certain properties could have a harder time getting insured in the future which could cause lenders to be unable to provide funding, Talerman said. He said Cape Cod 5 has even encountered situations where the bank was unable to provide a loan to a property with significant risk of coastal erosion.

“It’s going to continue to evolve,” he said. “The cost of insurance and the insurability of certain types of properties in certain types of locations, I think is going to become an issue. Without affordable insurance and adequate coverage, it gets awfully tough to get a loan.”

While residential lending was the focus of First Street’s report, Porter said that the effects of climate change could start to weigh on other areas of lending.

“On the commercial side, we’re finding a very similar problem, where insurance rates are increasing rapidly over the last five years and as those insurance rates are increasing, we are finding that operating expenditure side of the commercial world is starting to outpace revenues that are coming in,” he said. “All of a sudden, the cash flow that businesses and institutional investors are expecting to see from properties are not returning the same that they have in the past.”